Banks obtained the memo because of competition from money market funds.

Written by Wolf Richter of Wolf Street.

Money market funds have increased from almost 0% in April 2022 to over 5% since around April 2023, and Americans are liking this. a lot. As a result, banks are forced to compete for deposits by offering attractive interest rates on CDs. And Americans flocked to them, too.

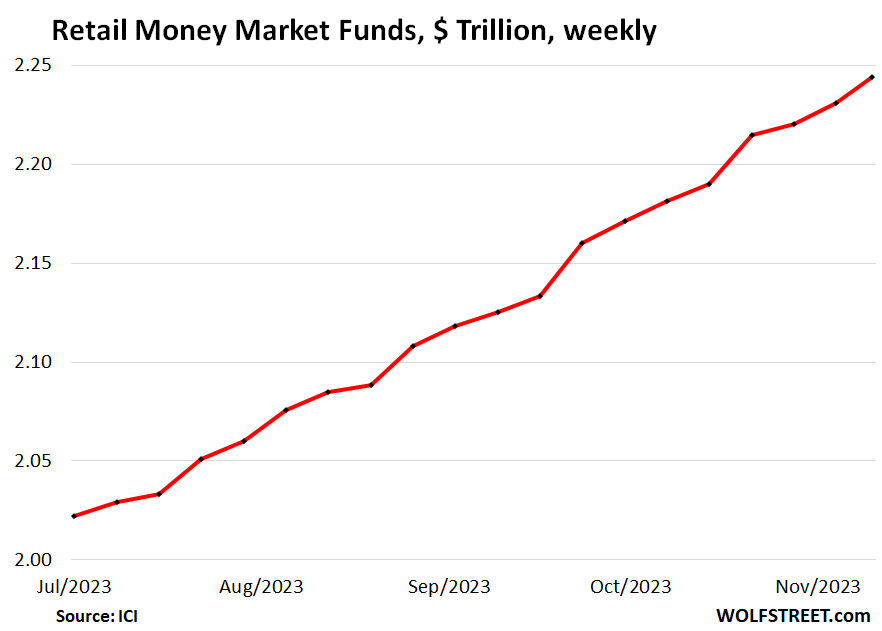

Money market funds for individual investors ICI (Investment Company Institute) reported on November 22nd that the amount increased by 0.6% from the previous week in the latest reporting week, by 2.5% in the past four weeks, and by 8.9% in the past three months to $2.24 trillion. A fund that invests in government products such as Treasury bills. A fund that invests in tax-exempt securities. and prime funds that invest in non-Treasury assets.

These are just funds sold to retail investors. Money market funds (MMFs) are divided into two main categories in terms of target audience based on the wording of the prospectus. Let’s look at them individually.

- Funds sold directly to individual investors (pictured above)

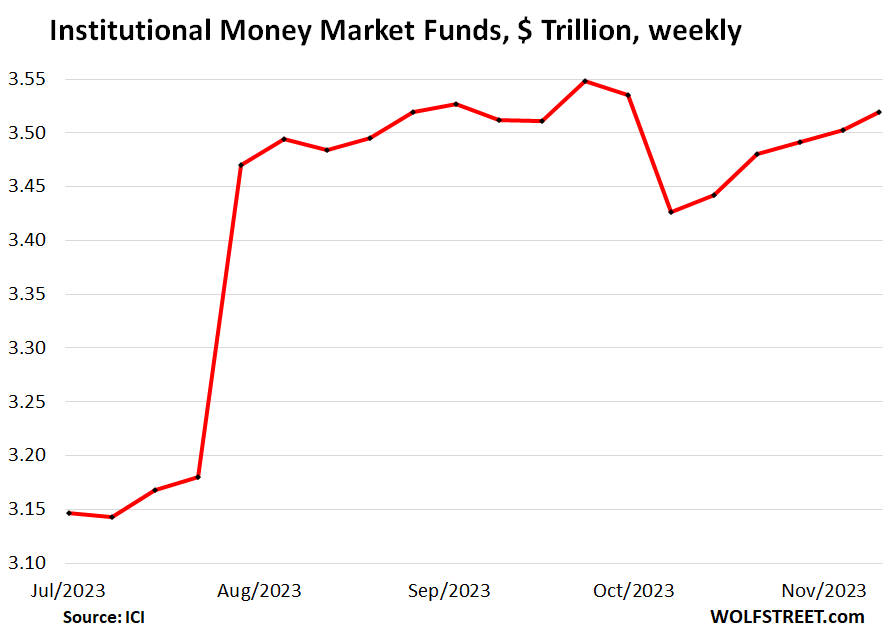

- Funds sold on behalf of customers, employees, and owners to institutions such as employers, trustees, and trustees (pictured below)

Money market funds (MMMFs) are mutual funds that invest in relatively safe short-term securities such as Treasury bills, repos, including what the Federal Reserve offers and calls “overnight reverse repos” (ON RRPs), high-grade commercial paper, and high-grade assets. is. -Commercial paper backed.

MMF for educational institutions It rose 0.5% last week and 2.2% over the past four weeks, but rose just 1.4% in the past three months after a sharp drop in October to $3.52 trillion.

Individuals are also indirectly included among the holders of these funds, as financial institutions include employers, trustees, or fiduciaries who purchase these funds on behalf of their customers, employees, or owners. Masu.

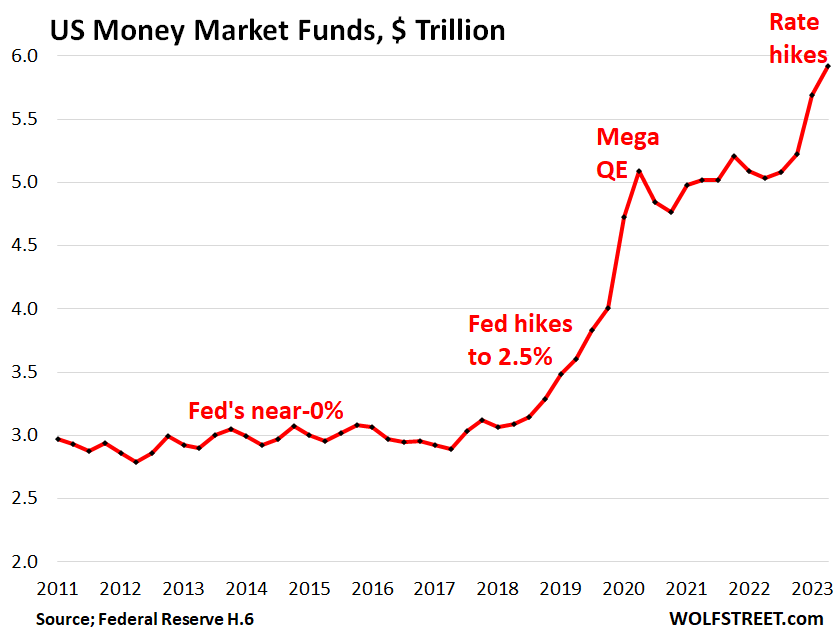

Total MMF balance It rose 2.3% over the past four weeks and 4.2% over the past three months to $5.76 trillion.

ICI only publishes data for the past 20 weeks, excluding ETFs and funds that invest primarily in other mutual funds.

The Fed releases slightly different metrics each quarter as part of its Money Stock Series, which are currently the same through the second quarter. You can see how the balance would balloon when the Fed first raised rates from 2017 to 2019, and then again this year with another big rate hike (data through Q2 only).

Money printing and money market funds. However, the chart above shows how the binge of money printing that began in March 2020 has created so much liquidity that money has flowed into money market funds even if the returns were close to 0%. And note that it caused a series of problems as these funds. They had to buy treasury bills, and the demand for treasury bills drove the yield on treasury bills down to 0% and even below 0%.

This has raised all sorts of concerns that some MMFs may be “losing money.” This is because an MMF’s 0% or negative income may not cover its fees and expenses, potentially causing the fund’s NAV to fall below $1, which could be a trigger. There will be a run on funds, forced selling by those funds, panic, contagion, and general schmearing.

This is why the Fed proposed overnight cash advance contracts (ON RRP) to MMFs. ON RRP actually pays interest and the Fed raised his RRP interest rate every time it raised interest rates. Here, we discussed the suggested retail price and the current plummeting balance.

Banks now have to compete with MMFs.

Deposits are loans made by bank customers to banks and form the basis of banks’ financing. As we’ve seen in sufficient detail at Silvergate Capital, Silicon Valley Bank, Signature Bank, and First, when depositors withdraw their money because they don’t like what they see or the interest they’re getting, and those deposits are drained. , banks can collapse. Republic.

So banks got the memo, offered CDs with yields of 5% or more, and savers flocked to them. A CD with a maturity date provides more stable funds than a savings or checking account, which allows you to withdraw cash instantly via electronic funds transfer.

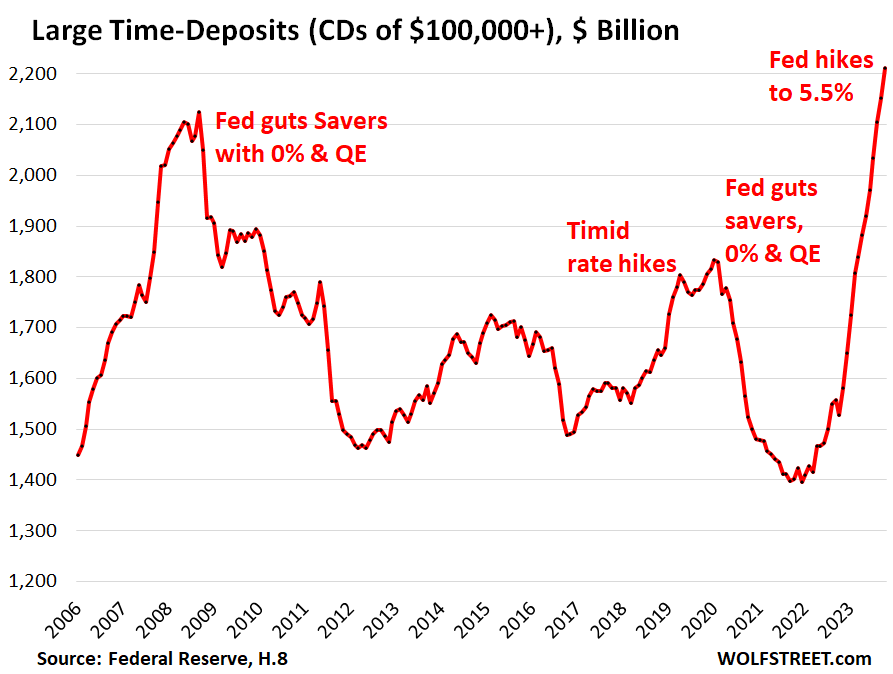

large fixed deposit – CDs of $100,000 or more – have soared 60% since the Fed began raising interest rates, reaching $2.1 trillion at the end of October from about $1.4 trillion in March 2022, according to Fed data.

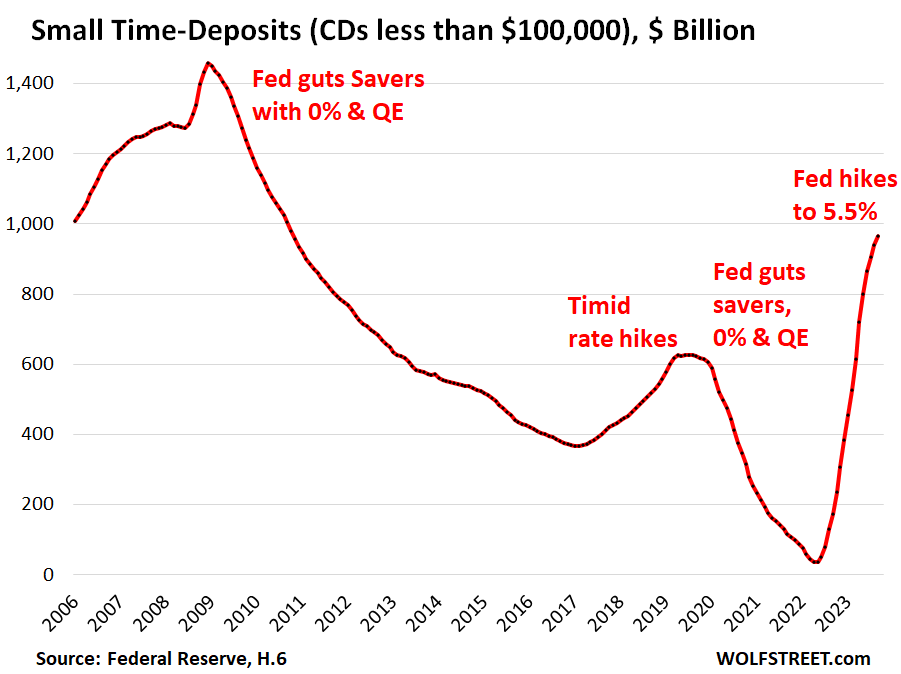

The Fed’s interest rate restraints during the financial crisis reduced the interest rates banks were paying on CDs to near 0%, sacrificing the cash flow of savers and other yield investors on the altar of asset price inflation. CD balances plummeted as most of the deposits went back into other types of bank accounts where no payments were made and balances continued to swell.

You can see the rhythm. The bearish interest rate hikes from December 2015 to December 2018 led to an increase in these term deposits. CD balances have plummeted due to the Fed’s interest rate controls since March 2020. Since interest rate hikes began in March 2022, CDs have become attractive again and investors have flocked to his CDs.

The bank provided a “brokered CD” To attract new deposits, they routed them through brokers to investors with brokerage accounts who were not necessarily customers of the bank, as existing deposits began fleeing the 0.1% interest rate banks were still paying. And reluctantly they stopped trying to screw over existing customers endlessly and started offering existing customers his 5% more CD to keep the deposit they still had.

Small term deposit – CDs under $100,000 – jumped from just $36 billion in May 2022 to nearly $1 trillion by the end of September, according to the latest data available from the Fed’s H.6 Money Stock Index . It is likely that the rise continued in October.

These small CDs reflect how ordinary people save, and now they can finally earn some income from investing, encouraging people to save a little more.

CDs are not the only bank savings products that have become more attractive due to their competitiveness with money market funds. Banks also offer higher interest rates on savings accounts, some as high as 5% or more, but unlike CDs, where the interest rate and funds are fixed until maturity, banks offer higher interest rates without notice. can be changed and the customer can withdraw funds. date.

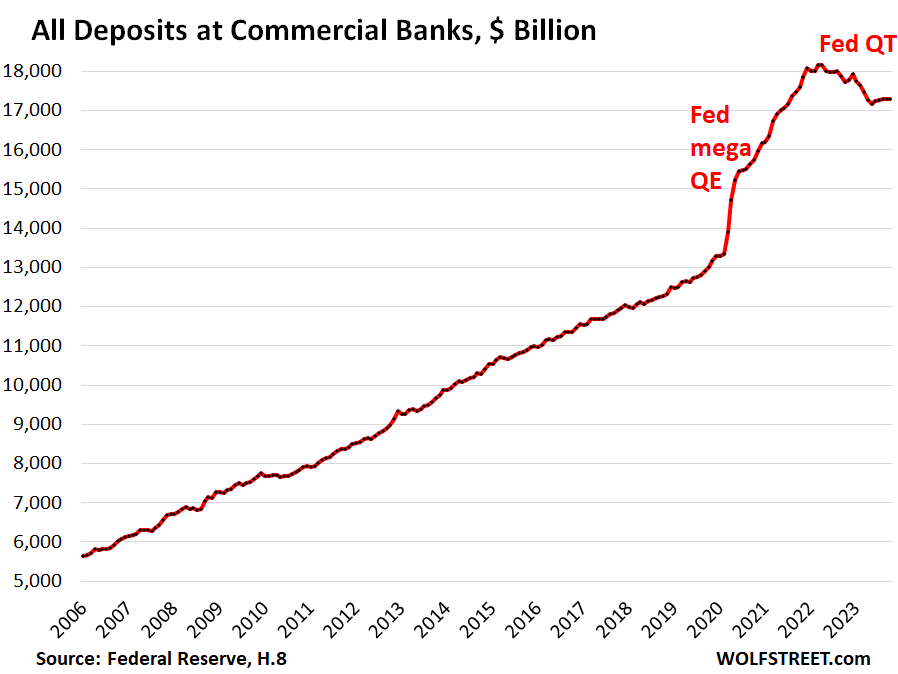

All deposits made by all commercial banks – Transaction accounts such as CDs, savings accounts, checking accounts, and corporate payroll accounts have declined by $890 billion from their peak in March 2022 to 17.3 billion due to the mass printing of large sums of money starting in March 2020. trillion dollars. They spike.

Enjoy reading and supporting Wolf Street? You can donate. I appreciate it very much. Click on the beer and iced tea mugs to see how.

Would you like to receive email notifications when new articles are published on WOLFSTREET? Sign up here.

![]()