")

Avdyachenko

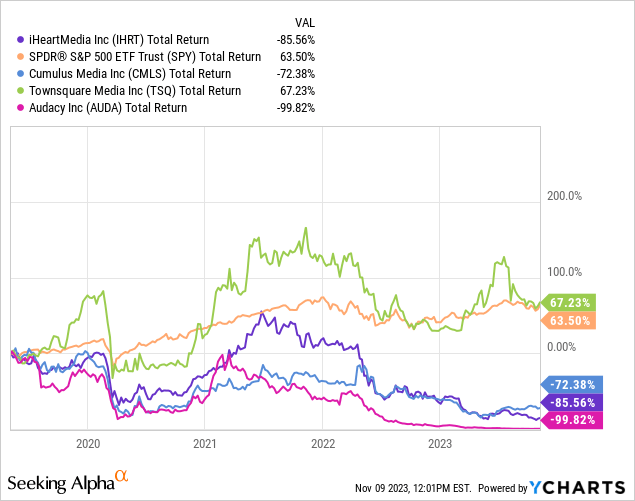

iHeartMedia (NASDAQ:IHRTSince then, IHRT stock has had a total return of -85.6%, making it a very disappointing investment. The S&P 500 achieved a total return of 63.5% over the same period.

IHRT has experienced a long-term decline in its core radio broadcasting business, which has also weighed on its closest peers Audacy (OTCPK:AUDA) and Cumulus Media (CMLS).

While IHRT has made significant strides towards focusing more on its digital business, its performance remains primarily driven by its core radio business.

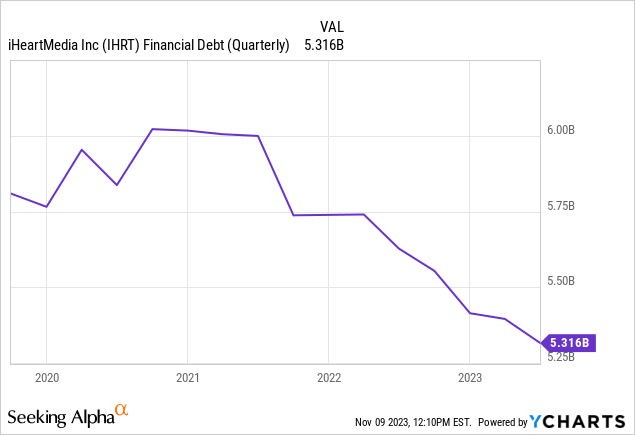

IHRT has struggled to emerge from bankruptcy with significant debt and significantly deleverage its balance sheet.

In my view, the challenges associated with declining core businesses and highly leveraged balance sheets are not likely to go away anytime soon. Therefore, I consider his IHRT an unattractive investment at current levels.

Company Profile

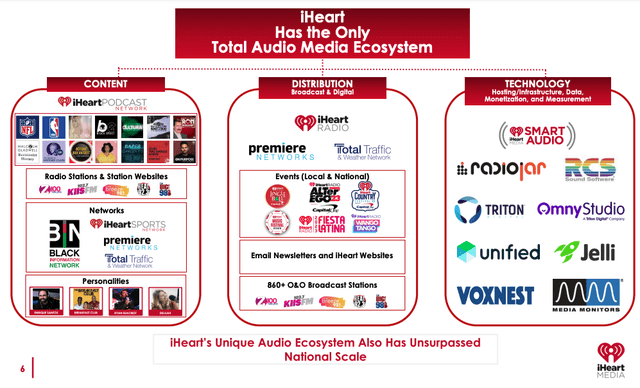

IHRT is the #1 audio media company in the United States based on total consumer reach. IHRT content can be heard on AM/FM broadcast radio stations, digital radio stations, satellite, the Internet, and through the iHeartRadio mobile application.

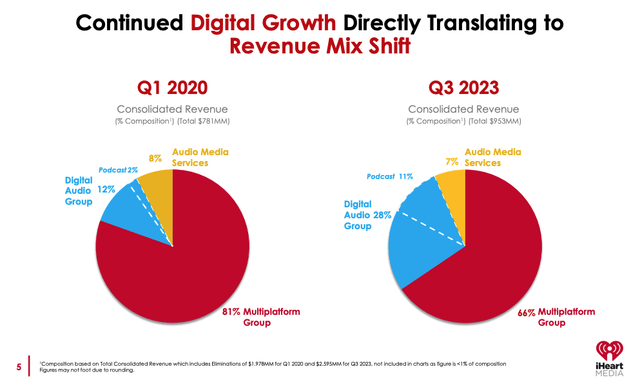

IHRT is divided into three segments: Multiplatform Group, Digital Audio Group, and Audio & Media Services Group.

The multiplatform group represents approximately 66% of total revenue and includes the company’s traditional broadcast radio, network, sponsorship and event businesses. The Digital Audio Group accounts for approximately 28% of total revenue and includes all of the company’s digital businesses, including podcasts. The Audio Media Services Group accounts for approximately 7% of revenues and includes media expression businesses, broadcast software, and scheduling services.

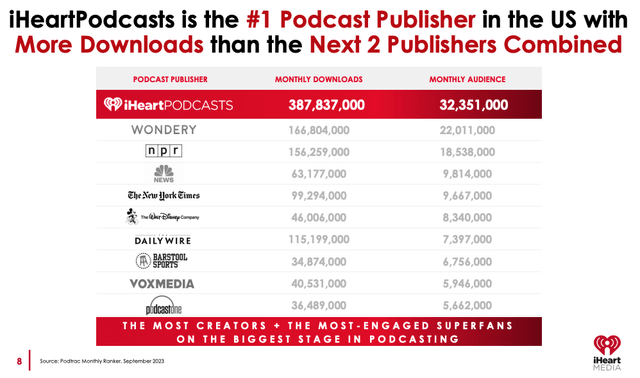

Over the past few years, IHRT has invested aggressively in its digital business and is now the number one podcast publisher in the United States with more downloads than the next two largest companies combined. Due to the growth of its podcast business, IHRT has significantly increased its share of digital revenue from approximately 12% in Q1 2020 to approximately 28% as of Q3 2023.

IHRT investor presentation IHRT investor presentation IHRT investor presentation

Traditional ratio business challenges

The traditional radio business has faced many challenges in recent years. The advent of digital alternatives such as podcasting has proven to be an attractive alternative to traditional AM/FM radio. Additionally, advertisers continue to prefer digital media over traditional media.

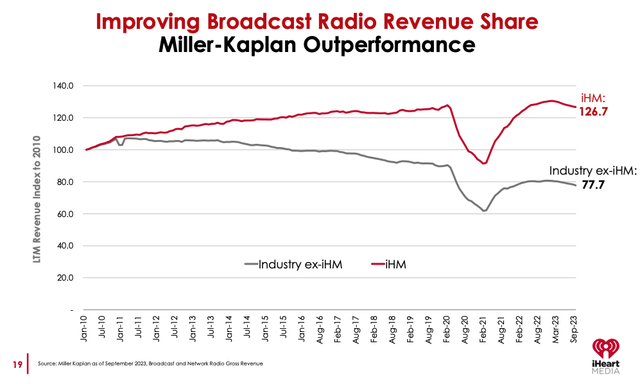

Despite these challenges, IHRT performed very well on a relative basis and captured broadcast radio’s revenue share. But despite increasing market share and growing its digital business, IHRT has struggled to generate consistent revenue growth. Additionally, IHRT has struggled to generate consistent revenue.

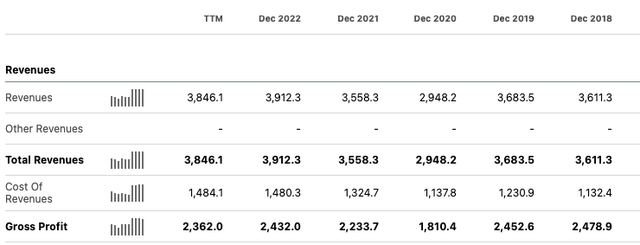

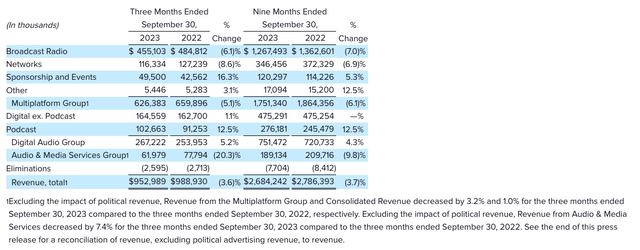

For the third quarter of 2023, IHRT reported total revenue of $952.98 million, down 3.6% year over year, and a net loss of $8.97 million. Multiplatform revenue decreased 5.1% year over year, but this was offset by a 5.2% increase in digital revenue. The company provided quarterly reconciliation reports. EBITD was $203.7 million (compared to $252.2 million in the prior year period). Adjusted EBITDA margin was 21.4%, compared to 25.5% in the prior year period.

IHRT also issued guidance calling for a high-single-digit (low-single-digit, excluding political impact) revenue decline in the fourth quarter. EBITDA is expected to be between $205 million and $215 million.

Investors were disappointed with the results, and IHRT fell by up to 10% after the results were announced.

IHRT investor presentation In search of alpha In search of alpha IHRT 2023 Q2 Financial Results Announcement

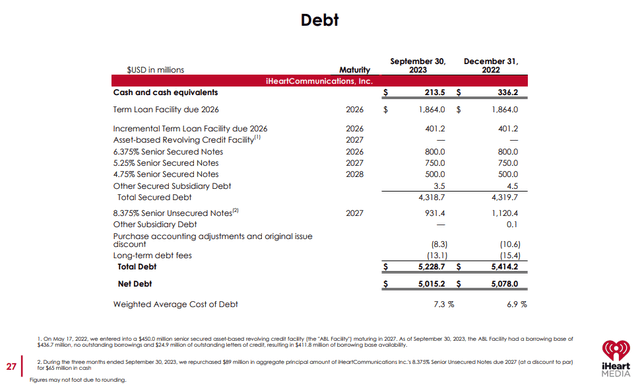

Highly leveraged balance sheet

As shown in the table below, IHRT has total debt of approximately $5.2 billion and net debt of $5.0 billion. On an LTM basis, IHRT generated adjustments. EBITDA was $804.1 million. Therefore, IHRT’s net leverage ratio is currently approximately 6.2x. This is clearly a high level for any company, and is particularly problematic for IHRT given the cyclicality and high volatility of earnings.

The company has said it is targeting a net leverage ratio of up to 4x, but it has a long way to go to reach that level from current levels. During the third quarter of 2023, the Company repurchased $89 million worth of 8.375% senior unsecured notes at a discount to par. The company also expects to generate $45 million in cash from the sale of its remaining radio towers, which will be used to repay debt.

In August, S&P downgraded IHRT’s credit rating from “B+” to “B” and gave a negative outlook.

The company’s weighted average cost of debt currently stands at 7.3%. This is quite low considering current interest rate levels, where the 10-year yield is around 4.6%. However, if companies are forced to refinance existing debt, the weighted average cost of debt is likely to increase.

The company has significant debt maturing in 2026, including a $2.26 billion term loan and $800 million in senior secured notes. Given the current capital market environment, it is unlikely that the company will be able to refinance this debt at reasonable interest rates.

IHRT investor presentation

evaluation

IHRT’s consensus earnings in 2024 is 7.5x. In contrast, his 2024 consensus earnings for the S&P 500 trades at about 18 times.

Although IHRT looks relatively cheap, it’s important to note that 2024 is a presidential election year, so IHRT’s returns should be significantly higher than in a normal year. IHRT has historically had very volatile earnings (even on a smoothed basis), making it very difficult to predict the company’s future earnings. Therefore, it’s hard to be bullish on the stock given the uncertainty about future earnings.

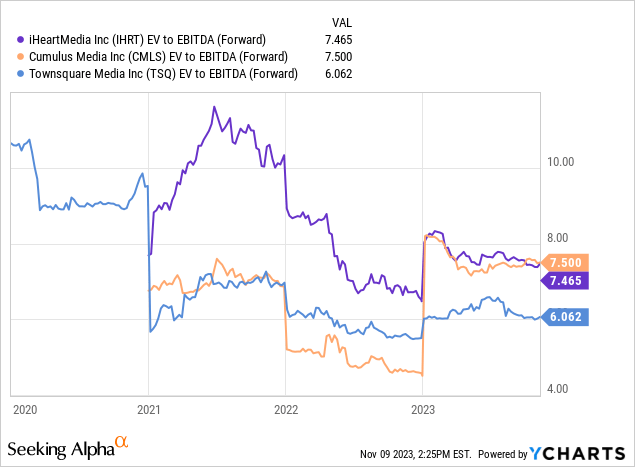

IHRT appears to be trading at roughly the same level as peers Cumulus Media (CMLS) and Townsquare Media (TSQ).

Potential upside factors

While long-term factors and a highly leveraged balance sheet are clear challenges for IHRT, the company has some positive investment potential.

Potential acquisition target

IHRT’s strong digital business makes it a potentially attractive acquisition target for many companies. In 2018, when IHRT was in bankruptcy, Apple (AAPL) explored Buy stock in the company to strengthen its streaming service. IHRT could also be a potential acquisition target for SiriusXM Holdings (SIRI) or Spotify (SPOT). While I believe that IHRT may be attractive to other companies, I believe that IHRT’s significant debt will make it significantly more difficult to transact outside of bankruptcy court.

Digital business growth

While IHRT’s traditional radio broadcast business is struggling, its digital business has demonstrated the ability to grow despite a difficult advertising environment. Digital business accounts for just 28% of his IHRT’s total revenue, but accounts for nearly 46% of his adjusted value. Adjusted EBITDA for the business is much higher. EBITDA margin vs. multiplatform business (35% vs. 25.9%) Digital streaming companies like Spotify trade at much higher valuations (58x 2025 revenue) compared to traditional radio companies . If IHRT is able to transform into a digital-focused company, its valuation could be revalued.

conclusion

IHRT has been unable to generate significant returns for shareholders since emerging from bankruptcy in 2019.

IHRT’s core radio business faces long-term challenges due to increased competition from digital players and the shift in advertising from traditional to digital media. These headwinds are especially difficult for his IHRT, as it is heavily in debt and has little margin for error.

2024 is expected to be a very strong earnings year for IHRT due to the election. IHRT stock appears to be trading at an attractive valuation of 7.5x 2024 consensus earnings, but future earnings are difficult to predict.

We believe the structural headwinds currently facing IHRT will further accelerate in the coming years, and we are concerned about the company’s ability to generate profits beyond 2025. Additionally, the company has relatively limited margin for error given its very high debt burden and significant maturity in 2026.

For this reason, I am initiating coverage with a sell rating, but will consider upgrading the stock if the strength of its digital business improves its earnings outlook and the company is able to deleverage its balance sheet.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.